Futarchy's Minor Flaw

In my 1999 article “Decision Markets” (IEEE Intelligent Systems 14(3):16-19, May/June), I explained how decision-conditional market estimates could be used to advise decisions, a concept I soon called “futarchy” when applied to governance.

From the first I considered the “decision selection bias” problem, which is where price biases result from a 3 step sequence: (1) decision-conditional prices are set before (2) info may be revealed that may influence (3) the decision. I discussed it in a Oct. 12, 1999 GMU talk, in many subsequent talks, and in two papers eventually published in 2006, “Designing Real Terrorism Futures” (Public Choice 128(1-2):257-274, July) and “Decision Markets for Policy Advice” (Promoting the General Welfare, pp.151-173, Nov.). From that last paper:

To avoid this decision selection problem, persons with access to decision-maker information should be permitted to trade in these markets. Also, the timing of the key decisions should be clearly announced just before such decisions are made so that speculators trading then need not fear the decision will be based on future information.

I (& others) have also noted that prices conditional on random decisions also solve this.

On Aug 14., Dynomight wrote:

That’s the idea of Futarchy, which Robin Hanson proposed in 2007. Why don’t we? Well, maybe it won’t work. In 2022, I wrote a post arguing that when you cancel one of the markets, you screw up the incentives for how people should bid, meaning prices won’t reflect the causal impact of different choices. I suggested prices reflect “correlation” rather than causation, for basically the same reason this happens with observational statistics. This post, it was magnificent. It didn’t convince anyone. …

Gradually I discovered that essentially the same point about futarchy had been made earlier by, e.g., Anders_H in 2015, abramdemski in 2017, and Luzka in 2021. … I wrote another post called “Futarchy’s fundamental flaw”. … Robin Hanson wrote a response, albeit without outward evidence of reading beyond the first paragraph. …

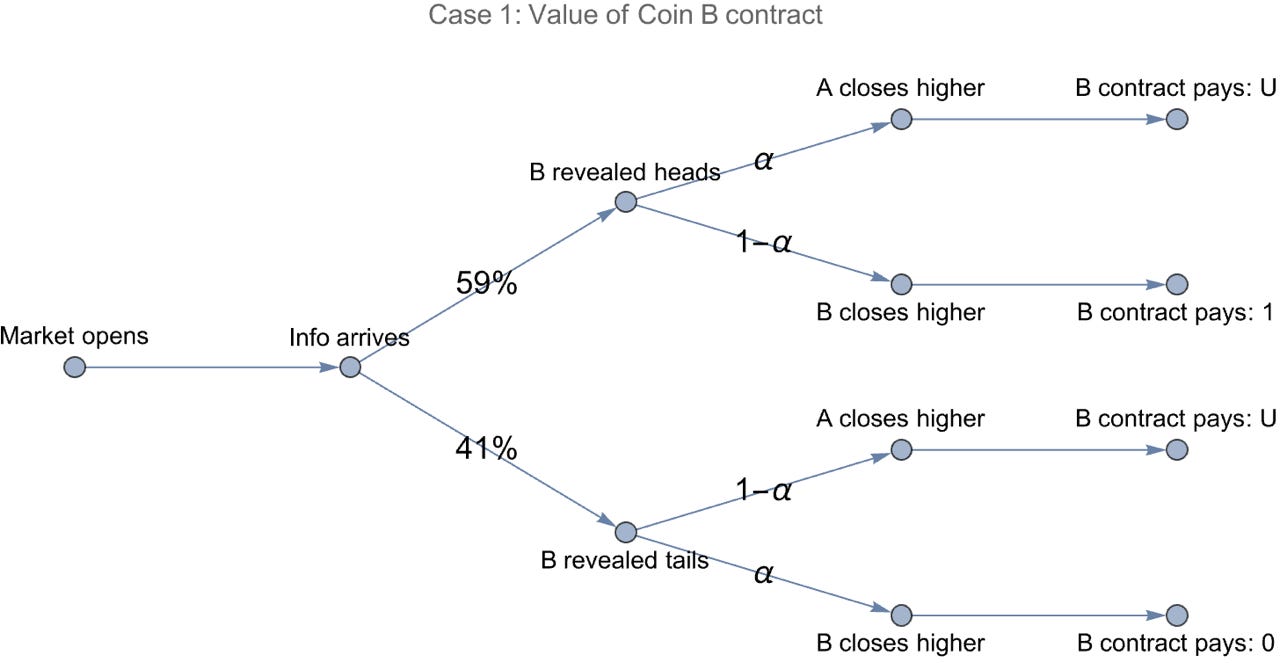

Bolton Bailey decided to stop theorizing and take one of my thought experiments and turn it into an actual experiment. … formalized this as follows: [Case 1:]

There are two markets, one for coin A and one for coin B.

Coin A is a normal coin that lands heads 60% of the time.

Coin B is a trick coin that either always lands heads or always lands tails, we just don’t know which. There’s a 59% it’s an always-heads coin.

Twenty-four hours before markets close, the true nature of coin B is revealed.

After the markets closes, whichever coin has a higher price is flipped and contracts pay out $1 for heads and $0 for tails. The other market is cancelled so everyone gets their money back. …

I was right. Everyone knew coin A had a higher chance of being heads than coin B, but everyone bid the price of coin B way above coin A anyway. …

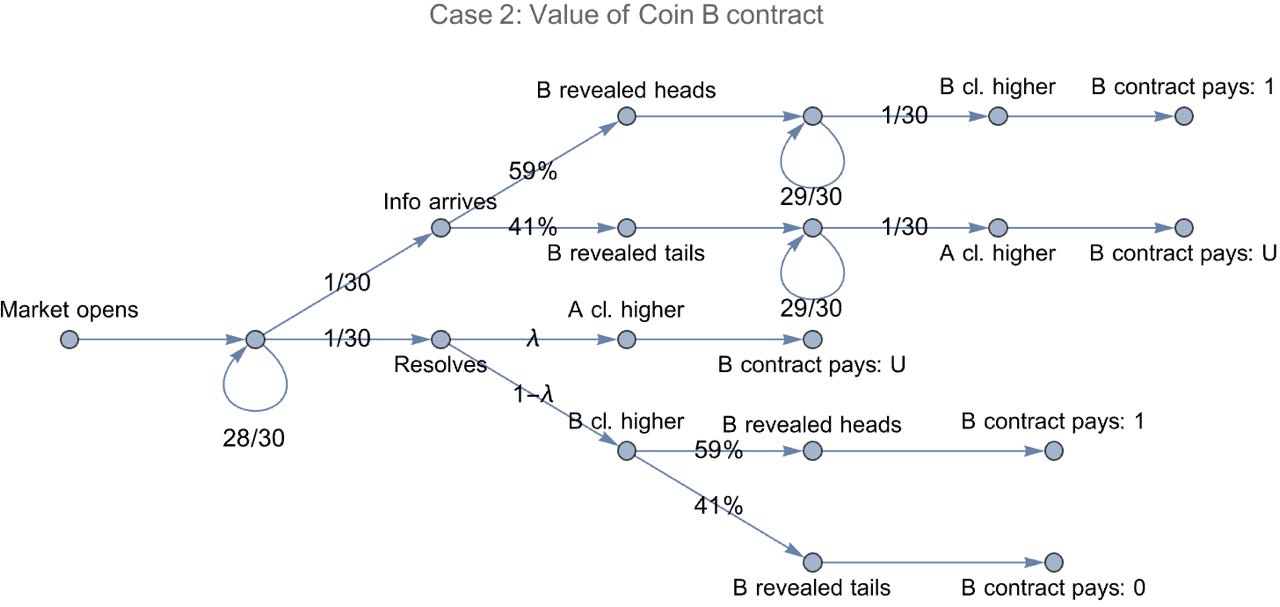

But prices did reflect causality when the market closed! … [However,] you can easily create situations that would have the same issue all the way through market close. Here’s one way you could do that: [Case 2:]

Let coin A be heads with probability 60%. This is public information.

Let coin B be an ALWAYS HEADS coin with probability 59% and ALWAYS TAILS coin with probability 41%. This is a secret.

Every day, generate a random integer between 1 and 30.

If it’s 1, immediately resolve the markets.

It it’s 2, reveal the nature of coin B.

If it’s between 3 and 30, do nothing.

My previous post, re which Dynomight suggests I didn’t read past his first paragraph, addressed the general oft-heard claim that decision markets reveal correlational, not causal, chances.

Here let me directly address the above two cases. I agree that they both generate conditional prices greatly biased away from the unbiased price of 59¢, in the second case for prices that appear just before the decision. It would indeed be a mistake to base decisions on naive interpretations of such prices.

My key point, however, is that both of these cases involve the problematic decision selection bias sequence listed above: (1) price, (2) info, (3) decision. And as discussed above, it seems quite feasible to avoid this problem in practical futarchy applications.

To convince you that I’ve paid attention here, I offer decision trees and price solutions for these two cases, calculated and drawn with assistance from Daniel Martin.

Here’s the decision tree for Case 1:

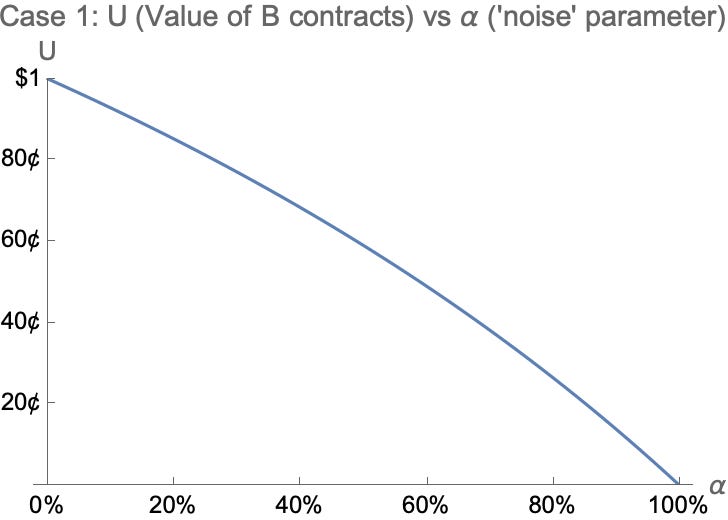

Note how this directly encodes the problematic sequence of price, info, decision. Note also that this assumes for convenience the same deviant choice rate α for both H and T branches. This tree implies this equation for the initial price U of the B contact:

And here is the implied relation between values of U and α:

For low noise α, this price is far above the unbiased price of 59¢.

Here is the decision tree for Case 2:

Again, this shows the key problem sequence of price, info, decision, though this time limited to the upper branch of the tree. This tree sets both of the deviant choice rates in case 1 to zero, as those now seem negligible compared to the rate λ of how often the A price closes higher. Here is the implied relation between U and λ:

And here is the implied relation between values of U and λ:

This graph clearly shows B contract price staying well above the unbiased price of 59¢.

So yes, futarchy can indeed give biased decision-conditional prices if one allows decision selection bias sequences of price then info then decision. Don’t do that.

But what if you are in a situation like case 2 above, where you aren’t sure when you will want to make your decision? Break that choice into a decision at each time-step. For example, in case 2, you could have a decision market just before each possible decision time with three options: coin A, coin B, or wait to decide later. Those markets would not suffer from a decision selection bias.

I still suggest you rename your idea, but otherwise, smart :)

It doesn't look like you link to the quoted August 14th post, which is at https://dynomight.net/futarchy-market/