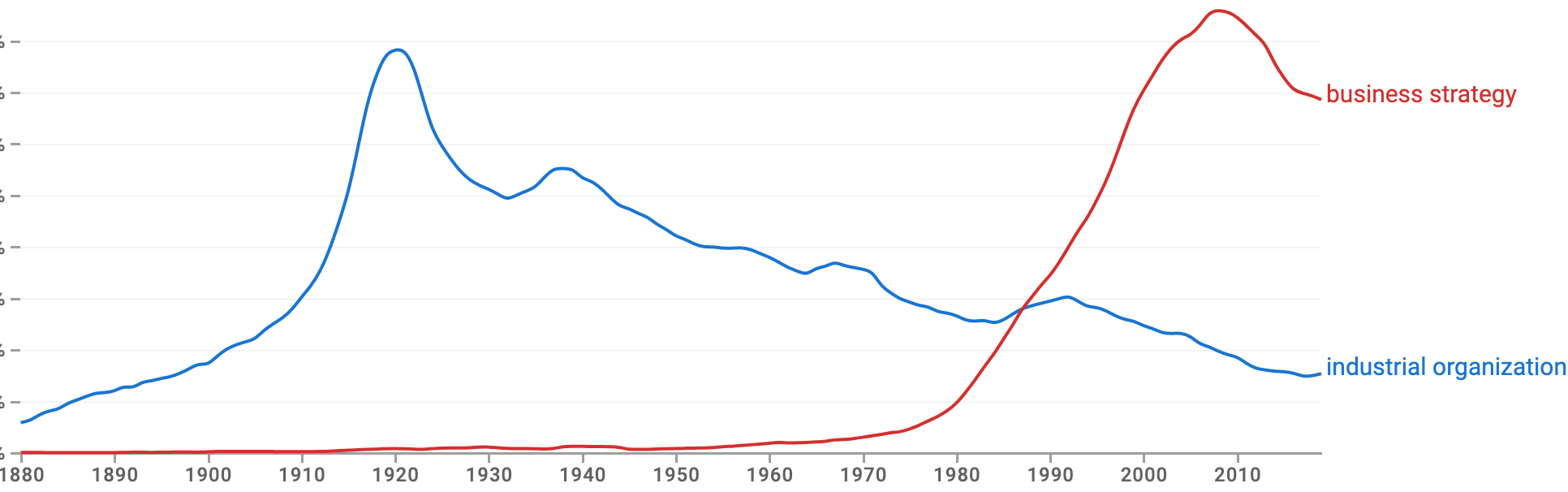

Hail Industrial Organization

(ngrams)

Economists know many useful things about human social behavior, and about how to improve it. And the world would probably be better off if it listened to economists more. But while the world respects economists enough to mention when their analyses support favored policies, people are much less interested in deciding what to favor based on econ analyses. What could get people to listen more?

There are many relevant factors, but a big one where we might do better is: a track record for being useful. For example, the world listens to chemists, computer scientists, and engineers in part because of their widely-known reputations for having long track records of being directly and simply useful to diverse clients.

Yes, econ majors in college are among the best paid outside of computers and engineering. But that may only show that learning our methods is an impressive feat, not that we produce reliable results. And the fact that people like to point to our analyses to support their policies only shows that we have prestige, not that we are right. What we want is a track record of being, not just impressive, but directly and clearly right, and useful because of that.

Now it turns out that we economists have actually found a way to be frequently and directly useful to diverse clients, and via being right, not just impressive. But we’ve failed to claim sufficient credit for this, and now we seem to be dropping the ball in pursuing it. This place is: business strategy.

When a firm considers what products or services to make, what customers to seek and how, and what prices to charge, it can help to have a theory of that firm’s industry. A theory of its customer demands and producer costs. A theory that says who wants what, who can take what actions when, who knows what when doing what, and how each actor tends to respond to their expectations re other actions. With such a theory, one can predict which actions might be how profitable, and choose accordingly.

Firms today regularly debate key business choices, and hire management consultants to advise those decisions. In addition, new firms pitch their plans to investors, and frequently revise such plans. And while all these choices might seem to be done without theories, that is an illusion. In fact, all such analyses are based on at least implicit theories of how local industries work. Such theories might be simple, or wrong, but they are there.

Now many aspects of useful industry theories are quite context dependent. But other aspects are more general. There are in fact many common patterns in key industry features, and in the ways that industries compete. And in the last century, the world has made great progress in developing better general theories of how firms compete in industries. Furthermore, economics has been central to that story.

In particular, game theory has become a robust general account of how social decisions are made. And we’ve identified dozens of key factors that influence industrial competition. Key ways in which industries differ, that result in different styles of competition. And we’ve worked out a great many specific models of how small sets of these factors work together to create distinctive patterns of industry competition. And much, perhaps even most, of this has happened within the econ field of “industrial organization.”

Today, most who discuss business strategy do so using concepts and distinctions that are well integrated into this rich well-developed and useful econ account of how firms in industries compete. And firms are in fact constantly reconsidering their business strategies using such concepts. So we economists have in fact developed powerful tools that are very useful, and are widely being used.

But, alas, we economists are failing to take credit for it. We don’t teach courses in business strategy, and we don’t recommend students who take our industrial organization courses for such roles. We’ve instead allowed business schools to do that teaching, and to take that credit. And even to take most of the consulting gigs.

Furthermore, academic economists have drifted away from industrial organizations; it is no longer in fashion. It mostly uses old fashion game theory, instead of now popular behaviorism or machine learning. It isn’t well suited for controlled experiments, which are so much the fashion in econ these days that all other kinds of data are considered unclean. And it doesn’t give many chances to promote woke agendas. So few people publish in industrial organization, and few students take classes in it. I know, as I still teach it, but to few students, and nearby universities don’t even offer it.

As usual, academic research priorities are mostly set by internal coalition politics, not by what would be good for the world as a whole, or even each field as a whole.

As a management consultant myself, I see how my profession often takes very basic theories from other firms and fields and repackages them in a way as to sell on the illusion that it is a "unique product provided by our firm". So Bain "invented" their ROS/RMS matrix as to not have to present the "BCG matrix" to their clients... McKinsey recommends "five big strategic moves", Strategy& talks about "Capabilities-Driven Strategy with How to Play and Right to Win" as if Roger Martin didn't exist... etc etc

So how could we make it better? There is no incentive to attribute credit for the underlying ideas, as no one else does it and clients are more interested in the final recommendation than in the whole idea genealogy anyway.

One idea I had was to make a consultancy that trawled and used ideas from any competitor, and entirely avoided this "thought leadership" arms race. Since ideas can be good or bad no matter where they come from, in this model being well-informed might make a difference... And economists with access to cutting edge ideas could be great partners.

The main impediment, however, is that consulting is mostly based on preexisting relationships. Really difficult to start a new firm unless you're an established partner with lots of connections, and if you're one of those there's not much incentive to change the business model and rock the boat.

US real GDP per capita has increased by about a factor of 4 since 1950. Then, why don't typical workers in the US have 4x the income? If we are producing 4x as much stuff per capita, who is getting all the stuff?