Futarchy Liquidity Details

The simple story about decision market liquidity is: such markets need an expectation of liquidity to induce traders to reveal info there, so that prices can usefully inform decisions. Thus those who value such advice should pay for it by subsidizing market maker liquidity.

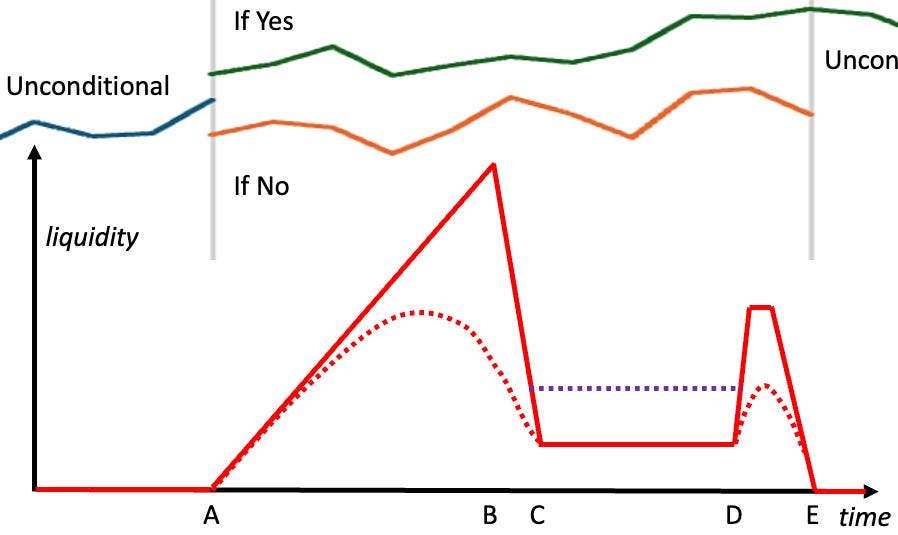

I’ve been thinking on this topic for the last few weeks, and in this post I’ll give a more complex story, tied to this diagram:

At the top of the diagram we see a simple decision market. On the left, at the earliest time, we see in blue the price of an unconditional market trading cash for an asset that pays in proportion to a key decision outcome, such as the stock of a firm or the coin of a DAO.

At time A, two conditional markets are introduced, shown in green and orange, also trading this asset for cash, but each conditional on some specific proposal being accepted (yes) or rejected (no). At time E the decision is made, based at least in part on price differences here between yes and no during the A to E period. At E one of the conditional markets, in this case yes, becomes equal to the unconditional market. The other conditional assets, in this case no, disappear.

In some uses of futarchy, there is no need for a no market, as the outcome given a no decision is obvious. In some uses of futarchy, the unconditional market doesn’t exist, as the outcome asset only exists to support this decision. But when an unconditional market exists along with two conditional markets, the three prices imply a probability of the decision being yes. The trading interface can let users make bets on that probability, via trades in these three markets. And that market chance of yes can be helpful in the rest of the system, as we will see.

In the lower half of the diagram we see a red line showing a plan for how conditional market liquidity provided by subsidized market makers changes with time. There is no liquidity before A or after E, as the conditional markets don’t exist then. At A, the conditional markets start, but with poorly informed initial prices created by the market system implementors. The first traders thus get to profit from correcting those first price mistakes, but they profit little as liquidity starts out near zero.

As there are games that traders can play if they can expect to be the only trader both before and after a sudden change in liquidity, it seems safer to just avoid sudden jumps, via have planned market maker liquidity be a continuous function of time. Also, information aggregation generally requires that traders can see and react to the trades of others, and thus the whole subsidized-trading process needs to last for long enough to have many rounds of traders seeing and reacting to the trades of others.

The profit that a trader makes from changing a price by delta, from the current price to their expected value of the asset, is the liquidity times that price delta squared (times the chance the condition will be met, for conditional markets). Thus adding more liquidity is offering a higher price for info. As decision market sponsors are likely a monopolist buyer of this info, they do not want to buy it at their value, but instead seek a monopolist profit-maximizing price lower than their info value, a price that trades off getting more info versus paying more for that info.

In the diagram, liquidity increases steadily from zero at A up to a maximum at B. Someone who is sure that they are a monopolist seller of some piece of info should thus wait until near B to reveal their info to the market. But those who expect that they are only the cheapest supplier of their info should worry that the second cheapest supplier will sell when the price rises to that second lowest cost. Thus the cheapest supplier should sell near the second cheapest cost. A predictably rising liquidity thus induces competition among those with access to the same info, allowing the decision market sponsor to buy that info for the lowest possible price.

The observation period between C and D is intended to show the clearest signal re the price difference between the yes and no markets, and thus be the main focus of decision makers seeking advice from these markets. As there are games that traders might play at the very end of the decision period D, it might be better to make D a random time, such as via a constant chance per time of switching modes.

We want to minimize both informed and manipulative trading during this observation period. Manipulators will focus on that period because decision makers will, but as manipulators try to look like informed traders, manipulators are easier to identify and counter when there is less informed trading then. We also want to reduce informed trading in this period as that can induce a decision selection bias earlier in this period.

Having a short observation period C to D, and a much higher subsidized liquidity both before and after the observation period, tempts informed traders away from the observation period, This difference needs to be big enough to counter the liquidity added by manipulators, shown in a purple dotted line. The liquidity should be higher before than after the observation period to make the decision as informed as possible. The higher liquidity in the period D to E before the conditional markets end also makes that a good time for traders to coordinate to exit these markets together if there are not thick unconditional market after E.

We want to minimize price noise in the observation period D to E not only to have a higher confidence in making the right decision, but also to allow the futarchy system to find and approve smaller policy changes. Futarchy can’t approve changes whose gains are smaller than some limit, and we want to reduce that limt.

As the sponsor pays to subsidize liquidity in decision markets to help inform their decision, such info is less valuable when their decision choice has become clearer. It can thus make sense to reduce liquidity provided by a factor of roughly p(1-p), where p is the market chance of a yes decision. Such a reduction is shown in the diagram as a dotted red line.

In an advisory futarchy, decision markets can consider the entire price history from A to E, and any other info they can find, in making their decision. The quality of the signal in the decision market prices of the period C to D will be highest if decision makers, or their informed associates, are allowed to trade in this period, if the decision time is clear, and if the period from C to E is short. It can also make sense to weigh price differences in the observation period by p(1-p), as conditional market prices may become less reliable as the chance of their condition becomes very small.

And there you have it, a more detailed analysis of how best a decision market sponsor can subsidize market makers to induce traders to reveal info there.

Added 20June: I worry about traders who follow this strategy: a) collect info, b) trade on it, c) tell the world about it, d) reverse their trade for profit. If they do step c) during the observation period C to D, that could add to a decision selection bias. We might want to discourage news and chat during the observation period.

ChatGPT4.5 guesses re financial market trader type distributions: ~15% of trades are informed, and ~10% of informed trader actively inform others after their trade. Trades needed within X sec according to this table of [range of delay X: % of informed, % of uninformed]: <0.01: 30%,10%, 0.01-1: 20%,10%, 1-100: 15%,20%, 100-1e4:15%,30%, 1e4-1e6:15,30%, >1e6: 5%,10%.

So many only a small fraction of informed trades might add price news during the observation period. Also, as median delay for informed trades is ~1.4min while median delay for uninformed is ~12hr, in general in financial markets uninformed traders should get lower trading costs by using periodic call markets.

Isn't this susceptible to silly trading strategies that are intended to extract the liquidity payment rather than genuinely trade?

For example, the delta^2 term might outweigh the value of the position itself and so selling for zero becomes beneficial. Preventing this puts a limit on the "liquidity" value, but I'm not sure there aren't still some silly outcomes possible.

What about selling back and forth between two cooperating traders?

Why is profit proportional to liquidity * delta^2?